Published on Sunday 30th November 2014 (AEST)

An article published on Seeking Alpha November 24th titled "Uranium Spot Prices Plummet as Buyers Exit the Market" is somewhat misleading and overlooks the nuances of the uranium spot market.

The spot market is thinly traded, driven primarily by one off transactions which can be very volatile (hence the 5% rebound last night bringing U308 spot prices back above $40/pound, after the 8% drop on Friday). Heightened focus on the spot move - on the pages of Seeking Alpha and elsewhere - spurred uranium equities such as Cameco Corp. & Denison to sell-off sharply, despite the fact that their uranium contracts are long term, and not directly related to the spot price on any given day.

The most important points to focus on when analyzing this market are the trajectory of uranium prices (higher), the long-term supply-demand imbalance (and why recent news regarding Japanese restarts is extremely important) and how much uranium-related equities are positioned to benefit given current valuations.

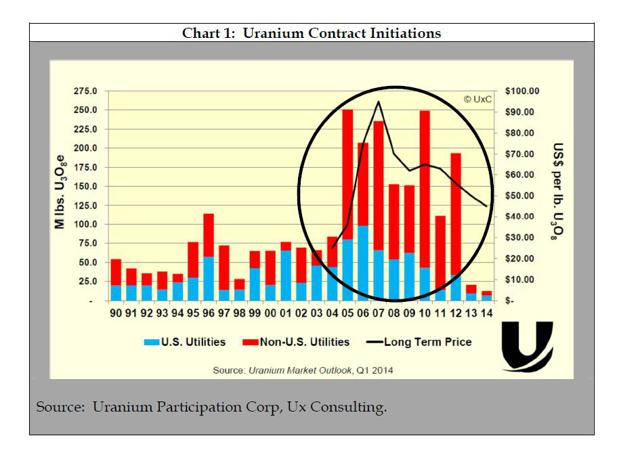

As stated above, the uranium market is not very deep - the buying trends of utilities is critical to the price and can drive large swings in the price on a one-off basis. Our channel checks suggest that most utilities are behind in striking new contracts supplying them with uranium, just as in aggregate, global utilities enter the biggest contract role cycle of the last several years (see Chart 1). Most contracts are executed on a five or ten-year basis, and as the chart shows, 2005 and 2010 were the heaviest volume years going back to 1990. We believe natural buyers will be in the market to support any dip in price (again, see last night's strong rebound) starting now through the first two quarters of 2015 to secure the supply they are behind in contracting.

(click to enlarge)

Most uranium-watchers are extremely focused on Japan, but why?

The Fukushima disaster was responsible for the start of the uranium

bear market, and many bulls have hung their hopes on Japanese

restarts as the primary driver of uranium equity prices. Earlier in

November, two reactors at Japan's Sendai plant received approval

for restart (the first since the 2011 Fukushima event). Though

important from a sentiment perspective, the restart of two reactors

in and of itself does not move the demand needle. The approval is

however, a game changer, but not for the reasons commonly

discussed. The decision to restart removes one of the biggest

short-term oversupply concerns affecting the market (another

catalyzing factor for global utility buying demand).

Prior to the Sendai announcement, many uranium market participants feared that an estimated 100mm pounds of Japanese inventory would be supplied to the market if Japanese officials failed in their campaign to restart. The likelihood of this event is now dramatically reduced as it would be illogical to sell necessary uranium reserves ahead of what will be a multi-year restart effort. As a sidenote, a successful snap election for Prime Minister Abe and his LDP party bodes well for an acceleration in the restart program. The LDP party has been firmly behind nuclear restarts, but their junior coalition partner, the Komeito party, has been an opposition force. Abe looks to be in a good position to secure an outright majority, and the implicit uranium catalyst is not often cited by the market.

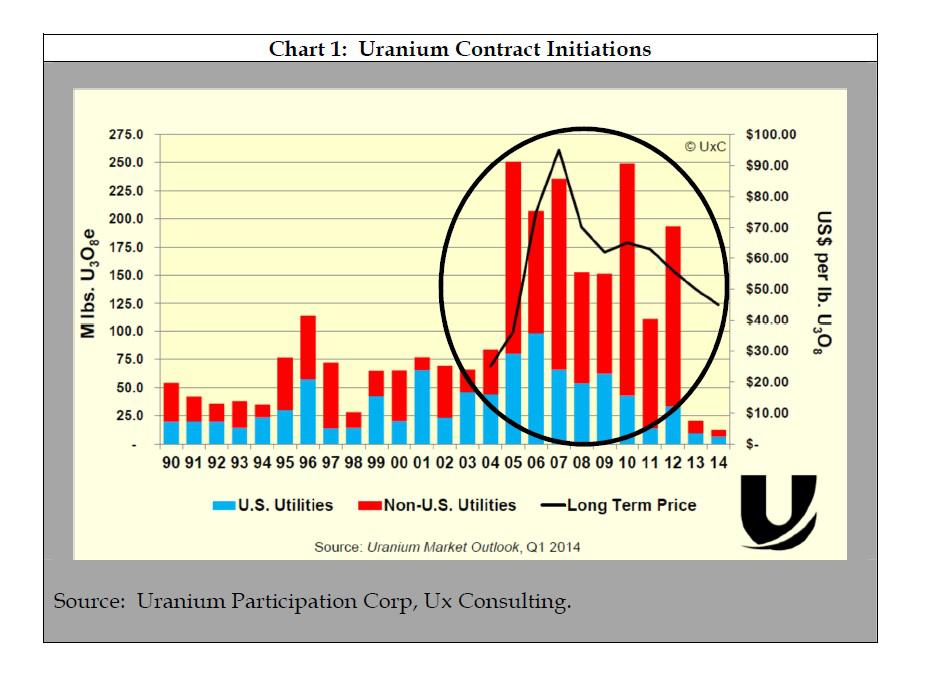

While Japan is a popular component of the uranium trade, its contribution to future demand becomes less significant when compared to the growing number of reactor builds in the rest of the world, which in aggregate are a much more important source of demand. Industry consultants and uranium company management teams alike project the uranium market going into deficit over the course of the next several years excluding the demand impact of Japanese restarts (see Chart 2). As has been pointed out many times by various sources, until spot uranium reaches some ~$75/pound, it is uneconomical for uranium supply to come online. We believe that a clearing price level of at least $75/pound will be achieved in Q1 or Q2 2015.

(click to enlarge)

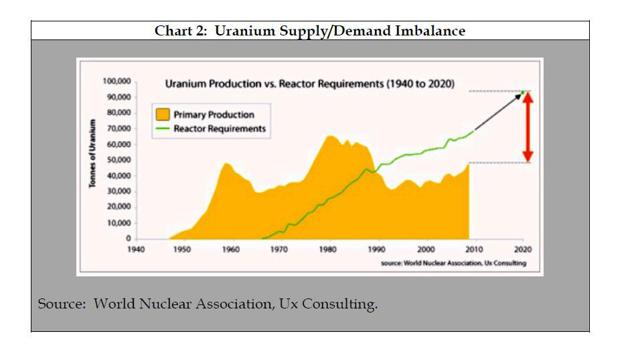

While the recent move in Uranium equities since the Sendai

reactor announcement may seem significant, it only brings equities

back to where they were trading at the end of September of this

year. Perhaps more surprising, is the general divergence between

the spot price and related uranium equities since the summer, which

has only partially closed (see Chart 3).

(click to enlarge)

Our discussions with bigger market players suggest that uranium demand is strong, while supply has been surprisingly thin. Meanwhile, both Cameco and Denison trade at significant discounts to NAV - upwards of 50% based on internal calculations based on given current pricing. We believe that higher spot prices, plus an eventual normalization of NAV multiples for the sector offers 100%+ upside to several names from today's prices.

Current equity prices reflect worst-case scenarios, just as the macro tailwinds for the industry are the strongest in several years. The buying behavior of utilities coming into their contract roll cycle, in addition to the positive sentiment catalyzed by Japan's restarts is underestimated by the market. Our top pick in the sector is Denison Mines based on the prospects of its Wheel Lake Gryphon zone drilling site, 22.5% joint venture stake of the Cigar Lake asset (operated by Cameco) and possibility of a near -term non-core asset sale (assets which currently have zero value in the NAV calculation). Internal one-year price target is C$ 2.20, implying greater than 75% upside from November 25th's closing price.

Click Image To Access Uranium Stocks Australia

.

Useful information shared. I am very happy to read this article. Thanks for giving us nice info. Fantastic walk through. I appreciate this post.

ReplyDeletemining companies utah

Blog looks very nice. Capture Media and communications Company offering b2b and b2c list services in India, USA and UK. I think best seo, ppc,smo,orm, like all digital marketing services and email database providers in Bangalore, USA,UK and India.

ReplyDeleteb2b and b2c database lists in Bangalore, Europe, UK, India

Email database lists in USA, Europe, UK, and India

Nice post, things explained in details. Thank You.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteI am extremely impressed along with your writing abilities, Thanks for this great share.

ReplyDeleteI am always searching online for tips that can benefit me. Thanks!

ReplyDeleteSuccess Accounting Group